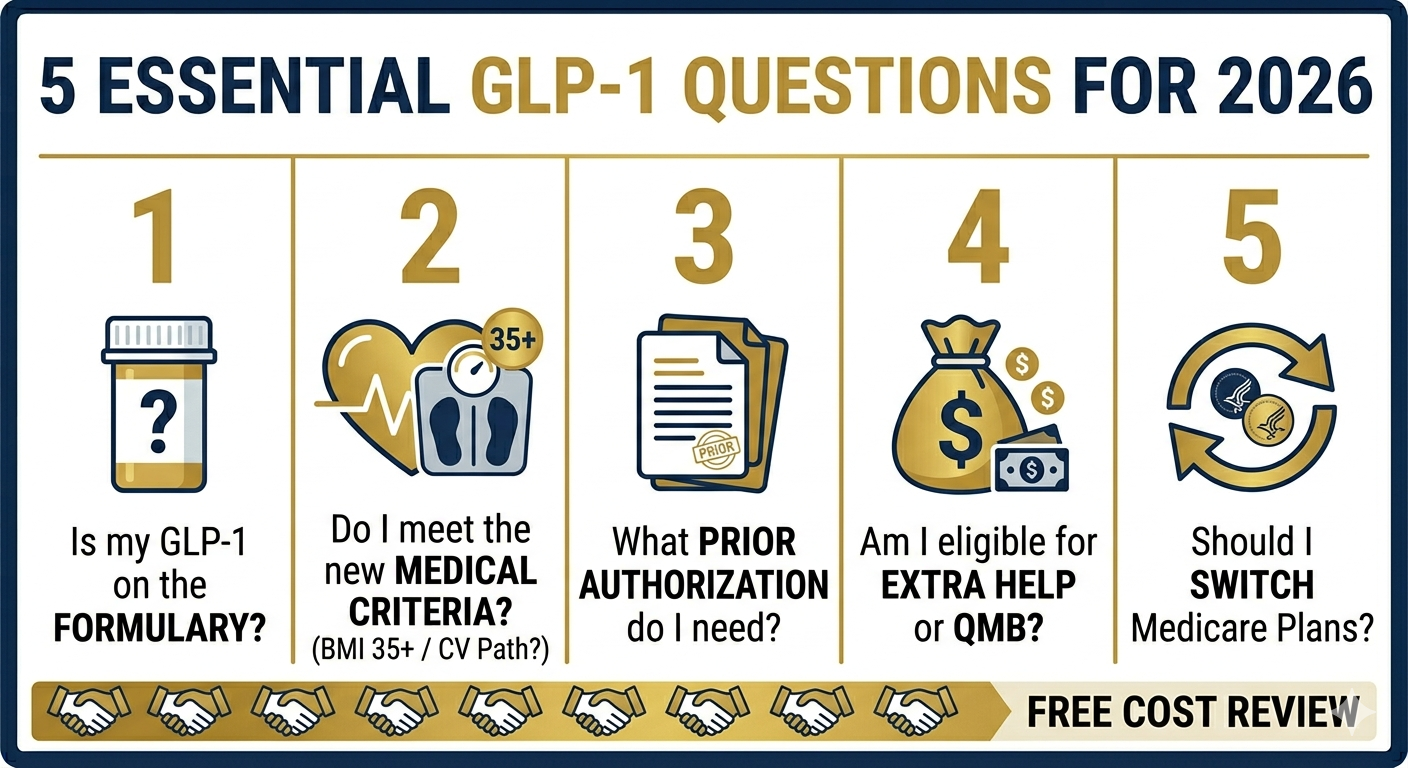

Question 1: Does My Current Medicare Plan Cover My Specific GLP-1 Drug?

This is the first and most important question. Medicare coverage of GLP-1 drugs does not mean every plan covers every GLP-1 drug. Each Part D plan has its own formulary — a list of covered medications — and GLP-1 drugs can vary significantly in their placement, availability, and cost from one plan to another.

How to get the answer:

- Log into your plan's website and search the formulary for your drug by name

- Call the Member Services number on the back of your insurance card

- Ask a Medicare agent to look it up for you across multiple plans

If your drug is not on the formulary, you may be able to request a formulary exception. Your doctor will need to submit a letter documenting why the specific drug is medically necessary for you.

Tip: Always search for your drug by its brand name AND its generic name. Semaglutide is the generic for both Ozempic and Wegovy — but these are different formulations at different doses.

Question 2: Do I Officially Qualify Under Medicare's Criteria?

Medicare's 2026 coverage of GLP-1 drugs is tied to specific clinical criteria. You generally need to meet one of two pathways:

- BMI pathway: BMI of 35 or higher with at least one obesity-related condition (diabetes, hypertension, sleep apnea, etc.)

- Cardiovascular pathway: Established cardiovascular disease with a BMI of 27 or higher

Ask your doctor: 'Is my BMI and my diagnoses documented in a way that supports prior authorization for a GLP-1 drug?' This is a direct, practical question your doctor can answer — and it could make the difference between approval and denial of your prior authorization.

If your medical records don't yet reflect the right diagnoses or BMI measurement, your next office visit is the time to get that documentation in order.

Question 3: Will I Need Prior Authorization, and What Does That Involve?

Almost certainly, yes. Prior authorization is a standard requirement for GLP-1 medications under Medicare Part D. It means your plan must approve the medication before it will cover it.

What prior authorization typically involves:

- Your doctor's office submits a PA request with clinical notes supporting your diagnosis and BMI

- Your plan reviews the request, usually within 72 hours (24 hours for urgent requests)

- The plan issues a decision: approval, denial, or a request for more information

If you're denied, don't give up. You have the right to appeal. Ask your doctor to submit additional documentation or a peer-to-peer review (where your doctor speaks directly to the plan's medical director). Many denials are overturned on appeal.

Ask your doctor's office: 'Does your office handle prior authorization requests, or will I need to manage this myself?' Many practices have dedicated staff for this.

Question 4: Am I Missing Out on Any Programs That Could Reduce My Cost?

Even with coverage, GLP-1 drugs can be expensive. There are several programs that could significantly reduce what you pay — and many beneficiaries don't know they qualify.

Programs worth asking about:

- Extra Help / Low-Income Subsidy (LIS): Reduces Part D cost-sharing to nearly zero for qualifying beneficiaries. Income limits are higher than many people expect.

- Medicare Savings Programs: Arizona's AHCCCS may help pay your Medicare premiums and cost-sharing if your income and resources are within limits.

- D-SNP plans: If you're dual eligible (Medicare + Medicaid), a Dual Eligible Special Needs Plan may offer zero-cost or very low-cost GLP-1 coverage as part of a comprehensive benefit package.

- Medicare Prescription Payment Plan: Spread your Part D out-of-pocket costs across monthly payments instead of paying large amounts early in the year.

A licensed Medicare agent can screen you for all of these programs at no charge during a plan review.

Question 5: Should I Switch Plans at the Next Enrollment Period?

This may be the most strategic question of all. If your current plan doesn't cover your GLP-1 drug — or covers it at a very high tier — you may be able to switch to a better plan during the Annual Enrollment Period (AEP), which runs October 15 through December 7 each year.

During AEP, you can:

- Switch from Original Medicare + Part D to a Medicare Advantage plan (or vice versa)

- Change from one Medicare Advantage plan to another

- Change from one standalone Part D plan to another

When evaluating plans for GLP-1 coverage, look at:

- Whether your GLP-1 drug is on the formulary at all

- What tier it's placed on and what your cost-sharing would be

- The plan's prior authorization criteria for GLP-1 drugs

- The plan's network of pharmacies (including mail-order, which can reduce costs)

- Total estimated annual drug costs including premiums and cost-sharing

The right plan for a GLP-1 drug user in Arizona may look very different from the plan that's right for someone without these medications. A tailored plan comparison is worth the time.

Don't wait until you're sick to review your Medicare coverage. Annual plan reviews — especially after major changes to covered benefits — can save you significant money and stress.