Introduction

Imagine having health insurance with no safety net. A plan where one serious illness could wipe out everything you’ve saved for retirement. You’d probably think that sounds like some cheap, terrible policy. But what if I told you millions of Americans have this exact plan? That plan… is Original Medicare. And the most dangerous part is a detail most people don’t find out about until it’s way too late: Original Medicare has no out-of-pocket maximum.

Welcome. Today we’re getting real about a topic that is absolutely critical if you’re near or in retirement. We're talking about Medicare. For decades, it's been seen as the foundation of healthcare for American seniors. And while it does provide essential coverage, it is not the complete, bulletproof shield many think it is. The system has gaps, and falling into one of them can be a financial disaster.

We’re going to expose the financial dangers hiding just under the surface of standard Medicare—dangers that could quietly drain your retirement savings. The truth is, what you don't know about Medicare can really, really hurt you. We’re going to look at the numbers, walk through the different parts of the system, and reveal the one detail that can be the difference between financial security and potential ruin in your golden years. So, stick with me, because getting this right could be one of the most important financial decisions you ever make.

Section 1: The Unlimited Risk of Original Medicare

Alright, let's start with the basics: Original Medicare, which is Part A and Part B. Part A is your hospital insurance. If you’re admitted to the hospital, that’s when Part A kicks in. But it’s not free. For 2026, you’re looking at a deductible of $1,736 per benefit period. And it’s really important to know that a "benefit period" isn't a year. It starts the day you're admitted as an inpatient and only ends after you’ve been out of the hospital or a skilled nursing facility for 60 straight days. This means if you have the bad luck of being hospitalized twice in one year, but more than 60 days apart, you could be paying that $1,736 deductible all over again.

And that’s not all. After your deductible, Medicare covers your first 60 days in the hospital. But if you're there longer, you start paying a daily chunk of the cost. For days 61 through 90 in 2026, that's $434 per day. After day 90, you dip into your "lifetime reserve days," and your daily cost jumps to $868. Once those days are used up, you are on the hook for all costs.

Then you have Part B, which is your medical insurance for things like doctor visits, outpatient care, and medical equipment. For 2026, the standard monthly premium is $202.90, and there's a separate annual deductible of $283. After you pay that deductible, Medicare generally picks up 80% of the bill. You’re responsible for the other 20%.

That 20% is the single most dangerous number in all of Medicare. Why? Because there is no limit, no cap, and no ceiling on how high that 20% can go. Twenty percent of a $1,000 bill is one thing. But what about 20% of a $100,000 cancer treatment? That’s $20,000 out of your pocket. What about 20% of a half-million-dollar surgery? That’s a $100,000 bill landing on your kitchen table. This one detail—the lack of an out-of-pocket maximum—is the biggest financial threat to retirees on Original Medicare. It’s a massive hole in the safety net that can swallow a lifetime of savings.

Section 2: The First Solution - Medicare Advantage

Because of this unlimited risk, private insurance companies came up with ways to plug the holes. The first big alternative is called Medicare Advantage, or Part C. These are plans from private companies, approved by Medicare, that have to cover everything Original Medicare does, but they work very differently.

The biggest selling point for a Medicare Advantage plan is that it’s legally required to have an annual out-of-pocket maximum. For 2026, the highest this limit can be is $9,250 for in-network care, and many plans set their limits even lower. This means once you’ve spent that amount on deductibles and copayments for covered services, the plan pays 100% for the rest of the year. That’s a huge protection against the catastrophic costs you could face with Original Medicare.

On top of that, many Medicare Advantage plans bundle in prescription drug coverage (Part D) and offer extras that Original Medicare doesn’t, like some dental, vision, and hearing care. All of that convenience, often for a very low or even zero-dollar monthly premium, makes these plans incredibly popular.

But there are major trade-offs. That out-of-pocket maximum isn’t a magic shield. Your monthly premiums don't count towards it, and neither do prescription drugs or services the plan doesn't cover. The biggest trade-off, though, is the network. Most Medicare Advantage plans are HMOs or PPOs, meaning you have to use their list of doctors and hospitals. If you go out-of-network, it can get very expensive, or it might not be covered at all. These plans also often require you to get "prior authorization" for services, which can lead to delays or even denials of care your doctor says you need. There are documented cases of people being denied coverage for critical treatments, like brain surgery, forcing families into stressful appeals while a medical condition gets worse. This is the flip side of Medicare Advantage—you get the safety of an out-of-pocket max, but you might give up some control and freedom of choice.

Section 3: The Second Solution - Medigap

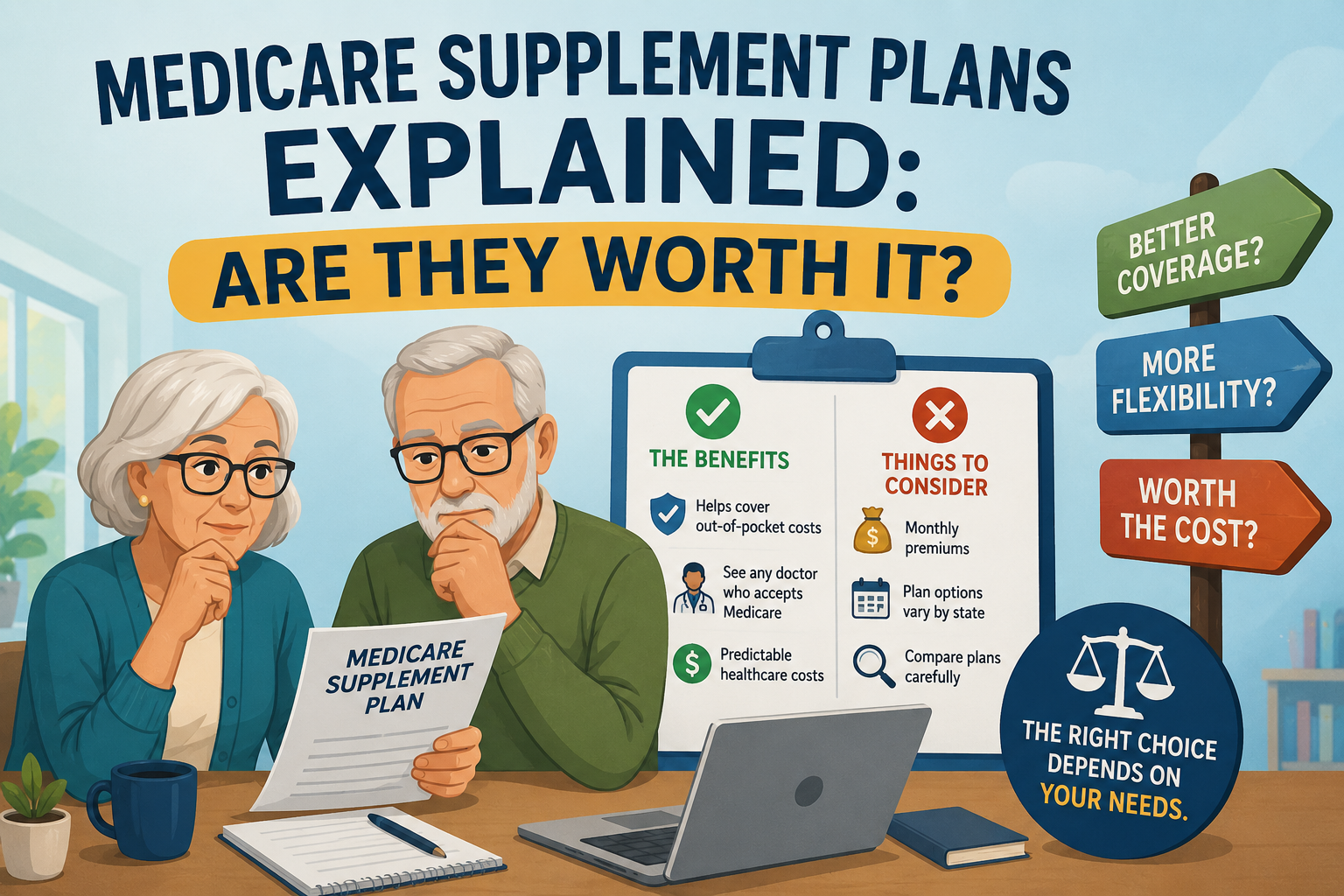

So what if you like the freedom of Original Medicare—being able to see any doctor or visit any hospital in the country that accepts Medicare—but you want to protect yourself from that unlimited 20%? There’s another path for that. It’s called Medicare Supplement Insurance, but most people just call it Medigap.

These are private insurance policies that work *with* Original Medicare; they don't replace it. A Medigap policy helps pay for the things Medicare leaves behind, like your deductibles and that scary 20% coinsurance. It’s important to know you can't have both a Medicare Advantage plan and a Medigap policy. You have to pick one or the other.

The great thing about Medigap is that the plans are standardized by the government. A Plan G from one company has to offer the exact same medical benefits as a Plan G from another company. The only differences are the price they charge and maybe their customer service. This makes it much easier to shop around and compare your options.

Basically, a Medigap plan’s job is to make your healthcare costs predictable. It turns the unlimited risk of Original Medicare into a fixed, manageable monthly premium. For a lot of people, that peace of mind is worth every single penny.

Section 4: Decoding Medigap - Plans and Costs

Medigap plans come in a few different flavors, labeled with letters like F, G, and N. If you became eligible for Medicare after January 1, 2020, Plan G is the most comprehensive plan you can buy. It covers almost everything Medicare doesn't, except for one thing: you have to pay the annual Part B deductible yourself, which is $283 in 2026. After you’ve paid that, Plan G takes care of the rest of the approved costs for the year.

Plan N is another popular choice that usually has a lower monthly premium in exchange for a little more cost-sharing. With Plan N, you’ll still pay the Part B deductible, and you might have small copayments for some doctor's visits (up to $20) or ER trips (up to $50 if you aren’t admitted).

Of course, this coverage isn't free. The average monthly premium for a Medigap plan in 2026 is about $149.50, but that can vary a lot depending on your age and where you live. A 65-year-old might find a Plan G for around $166 a month. By age 75, that same plan could cost over $205. If you want lower premiums, there are high-deductible versions of Plan G. In 2026, these plans require you to pay $2,950 out-of-pocket before the plan pays anything, but their monthly premiums are much lower.

There are also Plans K and L, which have their own out-of-pocket limits. For 2026, Plan K's limit is $8,000 and Plan L's is $4,000. You share costs with the plan until you hit your limit, and then the plan pays 100% for the rest of the year. The thing to remember is that Medigap costs go up as you get older, so you have to factor that rising cost into your long-term retirement budget.

CTA

Feeling a little overwhelmed by all the letters and numbers? That's totally normal. The Medicare system is complicated, and the stakes are high. But taking the time to really understand your choices is the first step to protecting yourself and your savings. To help you out, we’ve put together our medicare babe series. You can subscribe to our YouTube channel.

Section 5: The Gaps That Still Remain

Here’s a hard truth: even with a solid Medicare Advantage plan or a great Medigap policy, there are still major gaps in coverage that can leave you with big bills. The most common ones are dental, vision, and hearing.

Original Medicare doesn't cover routine dental cleanings or fillings, eye exams for glasses, or hearing aids. The impact of this is huge. Among low-income Medicare beneficiaries, studies have shown about 10% couldn't get the dental care they needed because of the cost. Another 8% couldn't get vision care, and 6% couldn't get hearing care for the same reason. And while a lot of Medicare Advantage plans offer some of these benefits, the coverage is often pretty limited.

Beyond those big three, there are other gaps people don't talk about as much. For example, Medicare has real weaknesses in its coverage for substance use disorder treatment, especially for things like residential treatment programs. This leaves vulnerable people and their families facing awful choices—either pay the full cost out-of-pocket or skip the care they desperately need. These aren't minor issues; they are essential health services that affect quality of life, and the lack of coverage creates a painful and expensive gap for millions of seniors.

Conclusion

As you can see, the idea that Medicare is a simple, all-in-one health plan for retirement is a dangerous myth. The reality is a complex maze of choices, trade-offs, and very real financial risks.

The single most important thing to take away from this is that Original Medicare by itself is not enough. That lack of an out-of-pocket maximum is a financial cliff you just don’t want to be anywhere near. This leaves you with a fundamental choice: Do you go with a Medicare Advantage plan, accepting the network rules and prior authorizations in exchange for a hard limit on your yearly costs? Or do you stick with the freedom of Original Medicare and buy a Medigap policy, paying a higher monthly premium to get predictable costs and get rid of that unlimited 20% risk?

On top of all that, you have to budget for the things that are almost never covered well, like dental, vision, and hearing. The real cost of Medicare gaps isn't just about money. It's about delayed care, impossible choices between prescriptions and groceries, and the slow draining of retirement savings that were supposed to give you security. Your golden years should be for enjoying the life you built, not for stressing about the next medical bill. The power to prevent that comes from getting informed and making a plan. Start today.