Navigating Long Term Care: Key Updates Medicare Seniors Need to Know

As we age, the prospect of needing long term care becomes an increasingly important conversation. For many Medicare beneficiaries, understanding what long term care entails, what Medicare covers, and the best ways to plan for future needs can feel overwhelming. The landscape of care options and financial planning is constantly evolving, making it crucial for seniors and their families to stay informed. As your trusted insurance advisor, we’re here to demystify long term care, highlight key considerations, and help you navigate the path to securing your future well-being.

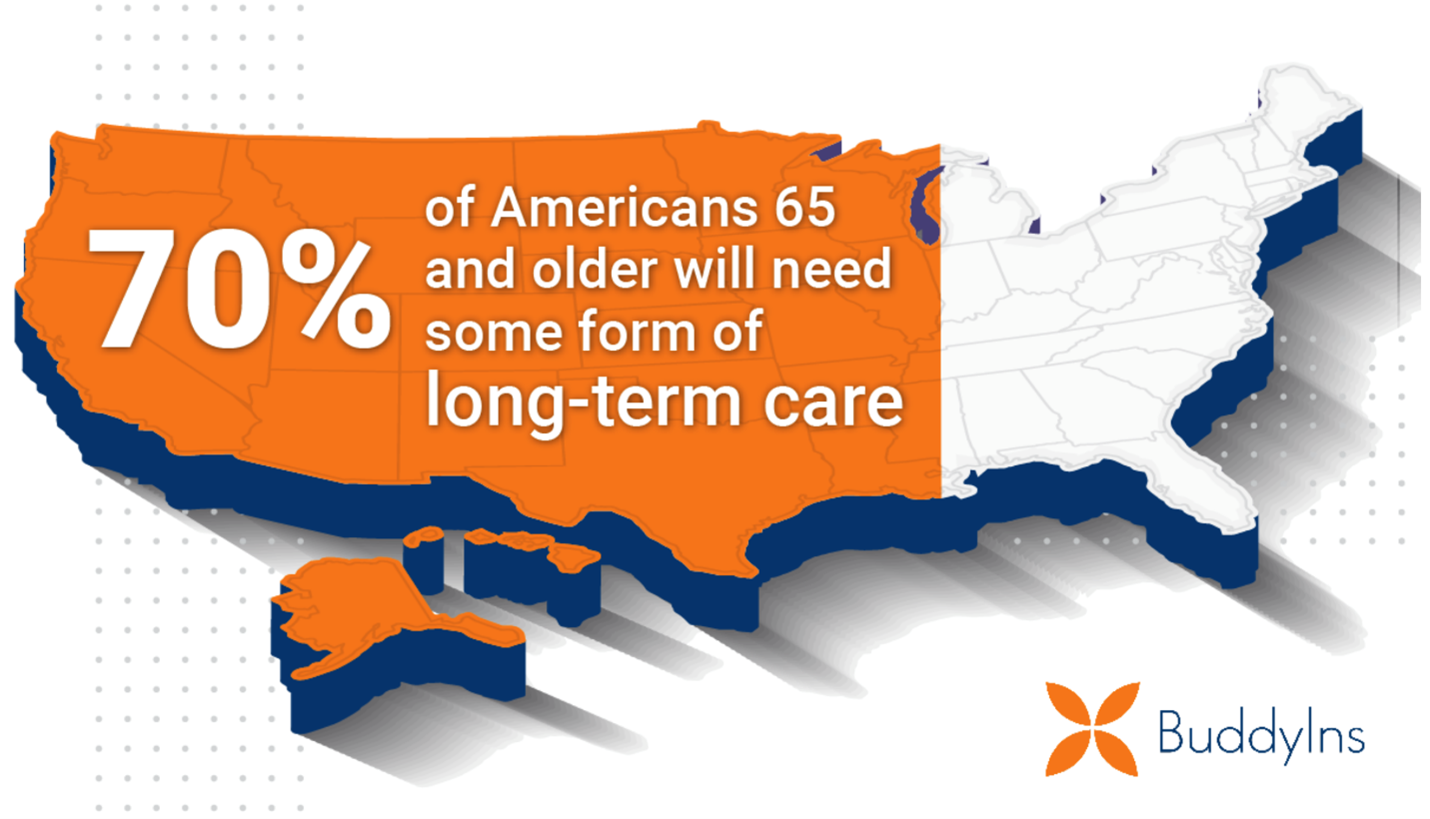

What is Long Term Care?

Long term care (LTC)

Refers to a range of services designed to help people live as independently and safely as possible when they can no longer perform everyday activities on their own. These services are typically needed due to chronic illness, disability, or cognitive impairment like Alzheimer's disease. Unlike short-term medical care, LTC is not about getting better; it's about assisting with daily life. Services can include help with Activities of Daily Living (ADLs) such as bathing, dressing, eating, continence, toileting, and transferring (moving in and out of a bed or chair). Care can be provided in various settings, including your own home, assisted living facilities, adult day care centers, or nursing homes.

Medicare's Role (and Limitations) in Long Term Care

This is perhaps the most critical distinction for Medicare seniors:

Medicare generally does NOT cover long term custodial care.

This is a widespread misconception that can lead to significant financial distress if not understood. While Medicare is an invaluable program for acute medical needs, its coverage for long term care is very limited:

In essence, Medicare focuses on *medical* care and *rehabilitation*, not on the ongoing support needed for daily living activities that define long term care. This leaves a significant gap that seniors must plan to fill.

The Soaring Cost of Long Term Care

The financial burden of long term care is substantial and continues to rise. According to recent data, the national median cost for a private room in a nursing home can exceed $100,000 per year, while a semi-private room is closer to $90,000 annually. Assisted living facilities can cost upwards of $50,000 per year, and even home health aide services can average over $60,000 annually for 44 hours of care per week. These costs vary significantly by location, but the trend is clear: without proper planning, long term care expenses can quickly deplete life savings and impact family inheritances.

Understanding Your Long Term Care Options

Given Medicare's limitations and the high costs, exploring dedicated long term care planning solutions is essential. Here are the primary avenues seniors consider:

Traditional Long Term Care Insurance

Traditional long term care insurance policies

are designed specifically to cover the costs of long term care services. These policies typically pay a daily or monthly benefit amount for a specified period (e.g., 3-5 years) once you meet eligibility criteria, usually based on your inability to perform a certain number of ADLs or cognitive impairment. Premiums are paid regularly, and benefits are tax-free in most cases.

Hybrid Life Insurance with Long Term Care Riders

A popular and growing option,

hybrid life insurance policies with LTC riders

combine life insurance (or an annuity) with long term care benefits. If you need long term care, you can draw on a portion of your death benefit or accumulated cash value to cover expenses. If you never need long term care, your beneficiaries still receive a death benefit. This "use it or lose it" concern often associated with traditional LTC insurance is mitigated with hybrid policies, making them an attractive choice for many.

Self-Funding

Some individuals choose to

self-fund

their long term care needs, relying on personal savings, investments, or assets. While this offers flexibility, it requires substantial wealth to cover potentially decades of care and carries the risk of depleting assets entirely. It's crucial to have a clear understanding of your financial resources and potential care costs if considering this path.

Medicaid

Medicaid

is a joint federal and state program that provides health coverage to low-income individuals. It is often the largest payer for long term care services in the U.S., but it is a "payer of last resort." To qualify for Medicaid's long term care benefits, individuals must meet strict income and asset limits, often requiring them to spend down most of their assets. This is typically not a proactive planning strategy but rather a safety net for those who have exhausted other options.

Key Updates and Considerations for Today's Planning

While Medicare's core long term care coverage hasn't seen dramatic "updates," the context in which seniors plan for LTC is constantly evolving. Here are key considerations:

The Rising Demand for Home-Based Care

A significant trend is the increasing preference for

home-based care

. Most seniors prefer to age in place, and modern LTC insurance policies,