Why Business Owners Need Life Insurance: Protecting Your Legacy and Your Enterprise

As a business owner, your dedication is unwavering. You pour your heart, soul, and often your personal finances into building something meaningful. You meticulously plan for growth, manage operations, and navigate market fluctuations. But amidst the daily demands and future aspirations, have you adequately prepared for the unexpected events that could threaten the very foundation of your enterprise? This isn't just about personal protection; it's about safeguarding your business, your employees, your partners, and your legacy. While many associate life insurance solely with family protection, for a business owner, it transforms into an indispensable strategic tool, offering far more than just a death benefit. It provides stability, liquidity, and even capital, ensuring that your business can thrive even if you or another vital member is no longer at the helm.

Understanding the Unique Risks of Business Ownership

Running a business, regardless of its size or industry, comes with a distinct set of risks that extend beyond typical personal financial planning. Your business is often intertwined with your personal finances, and the sudden loss of a key individual – whether it's you, a co-founder, or a critical employee – can send shockwaves through every aspect of your operation. This isn't merely an emotional blow; it's a potential financial catastrophe that can disrupt cash flow, cripple operations, damage credit, and even force the sale or liquidation of a thriving enterprise. Recognizing these vulnerabilities is the first step toward implementing robust protective measures, with life insurance standing out as one of the most effective solutions.

Key Person Insurance: Protecting Your Business's Core

Imagine your business as a complex machine. Some parts are easily replaceable, while others are absolutely critical to its function. In a business, these critical parts are often individuals – the innovators, the rainmakers, the strategic thinkers, the operational gurus. The sudden loss of such an individual can be devastating, and that's precisely where key person insurance (also known as key man insurance) comes into play.

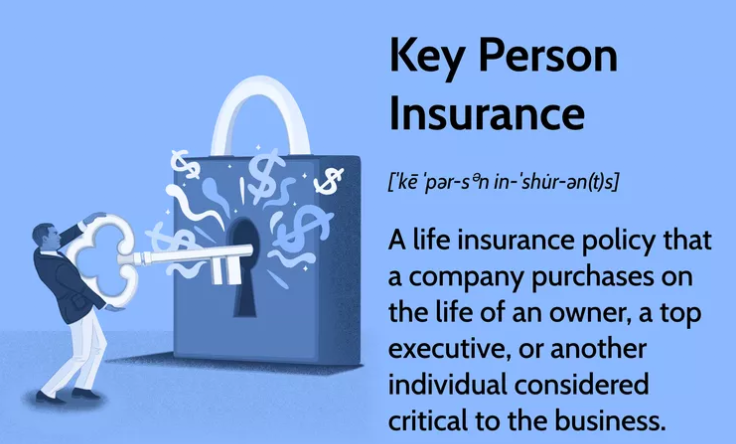

What is Key Person Insurance and Why is it Vital?

Key person insurance is a life insurance policy taken out by a business on the life of an employee whose death would cause significant financial harm to the company. The business is both the owner and the beneficiary of the policy, paying the premiums. If the insured key person dies, the business receives the death benefit, which is typically paid out tax-free. This type of policy is vital because it recognizes that certain individuals are irreplaceable in the short term, and their absence can lead to a cascade of problems: *

Loss of Revenue:

A top salesperson or client relationship manager might take significant accounts or future revenue opportunities with them. *

Operational Disruptions:

A lead engineer, product developer, or operations manager might hold proprietary knowledge or critical processes without which the business cannot function efficiently. *

Reduced Morale:

The loss of a respected leader can negatively impact employee morale and lead to further staff turnover. *

Damaged Investor Confidence:

Investors, lenders, and partners may lose faith in the company's ability to continue operations successfully, potentially withdrawing support or capital. *

Credit Impairment:

If the key person was a guarantor on business loans, their death could trigger default clauses, putting the company's credit and assets at risk.

Identifying Your Key Persons

A "key person" isn't necessarily just the CEO or founder. They could be: * **Founders or Co-Owners:** Especially in the early stages, their vision, leadership, and expertise are foundational. * **Top Sales Executives:** Individuals responsible for a significant portion of the company's revenue. * **Lead Engineers or Innovators:** Those with specialized skills or intellectual property that drives product development or service delivery. * **Financial Officers:** CFOs or controllers who manage the company's financial health and relationships with banks. * **Anyone with substantial knowledge of the busincess operations