Navigating Your Medicare Choices: Medicare Supplement vs. Medicare Advantage

Understanding Medicare can feel like deciphering a complex puzzle, especially when it comes to choosing between Medicare Supplement (Medigap) and Medicare Advantage (Part C) plans. These two distinct paths offer very different ways to receive your Medicare benefits, each with its own structure, costs, and coverage features. Making the right choice is crucial for your health and financial well-being, as it impacts everything from your monthly premiums to your out-of-pocket costs at the doctor's office, and even your freedom to choose providers. As an expert insurance professional specializing in Medicare, my goal is to demystify these options for you. This comprehensive guide will break down the fundamental differences between Medicare Supplement and Medicare Advantage plans, helping you understand how each works, what they cover, and who might benefit most from each type. By the end, you'll have a clearer picture, empowering you to make an informed decision about which path aligns best with your healthcare needs, budget, and lifestyle.

The Foundation: Understanding Original Medicare

Before diving into Medicare Supplement and Medicare Advantage, it's essential to understand what they build upon:

Original Medicare

. Original Medicare is government-funded health insurance for people aged 65 or older, certain younger people with disabilities, and people with End-Stage Renal Disease (ESRD). It consists of two main parts:

While Original Medicare provides robust coverage, it doesn't cover everything. There are "gaps" in coverage, such as deductibles, coinsurance, and copayments that you are responsible for. It also doesn't cover most routine dental, vision, hearing, or prescription drugs. This is where Medicare Supplement and Medicare Advantage plans come into play – they are designed to help fill these gaps or provide an alternative way to receive your benefits.

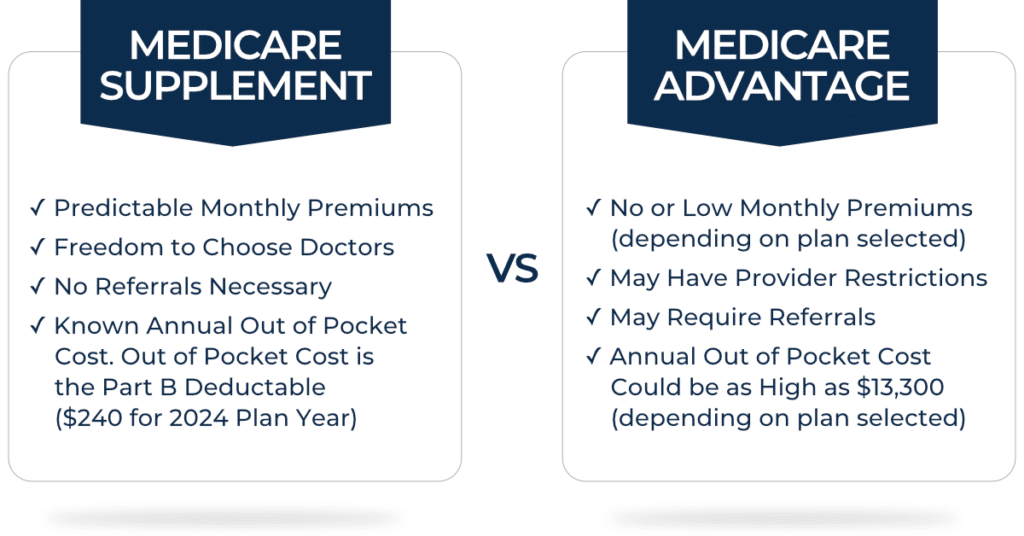

Understanding Medicare Supplement (Medigap) Plans

Medicare Supplement Insurance plans

, often referred to as

Medigap plans

, are sold by private insurance companies to help pay some of the healthcare costs that Original Medicare doesn't cover. These plans work

with

your Original Medicare, not instead of it.

How Medigap Plans Work

If you have Original Medicare and a Medigap policy, Original Medicare pays its share of the Medicare-approved amount for covered healthcare costs, and then your Medigap policy pays its share. This means you