Medicare Part D Explained: Making Informed Choices for Prescription Coverage

Navigating Medicare can feel like deciphering a complex puzzle, and nowhere is this more true than with prescription drug coverage. For millions of Americans, prescription medications are a daily necessity, making **Medicare Part D** an absolutely critical component of their healthcare plan. Choosing the right Part D plan isn't just about saving money; it's about ensuring you have access to the medications you need, when you need them, without unexpected financial burdens. This guide will demystify Medicare Part D, empowering you to make informed choices for your prescription coverage.

What is Medicare Part D?

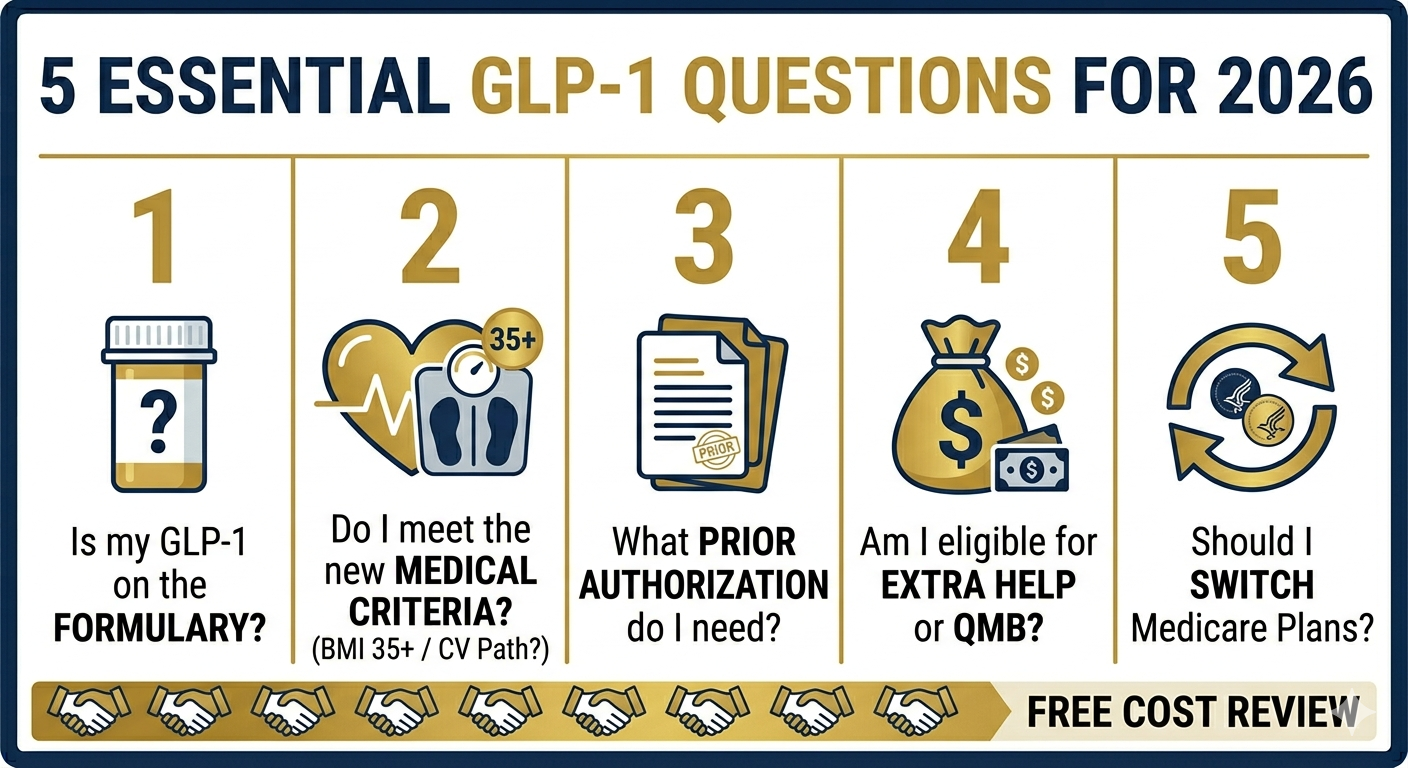

Medicare Part D is optional prescription drug coverage offered by private insurance companies approved by Medicare. These plans work in conjunction with Original Medicare (Parts A and B) or can be included as part of a Medicare Advantage (Part C) plan that offers prescription drug coverage (MAPD). Part D helps cover the costs of prescription drugs, but plans vary significantly in terms of their formularies (lists of covered drugs), deductibles, copayments, and preferred pharmacies.

Key Considerations for Choosing a Part D Plan

Selecting the optimal Part D plan requires careful consideration of several factors unique to your situation. Here’s how to approach it strategically:

Your Prescription List is Your Starting Point

The most crucial step in choosing a Part D plan is to **review all your current prescriptions**. This isn't just a recommendation; it's the cornerstone of finding the right fit. Every Part D plan has a **formulary**, which is its list of covered drugs. A drug that's covered by one plan might not be covered by another, or it might be in a different cost-sharing tier, leading to vastly different out-of-pocket costs. Here’s how to effectively use your prescription list:

By entering your actual prescriptions into the Plan Finder, you move beyond guesswork and get a clear picture of which plans truly offer the best value for *your* specific needs.

Pharmacy Network Matters

Just as important as your prescription list is ensuring that the pharmacy you use is **in-network** with your chosen Part D plan. Most Part D plans have a network of pharmacies, and you'll typically pay less for your medications if you use a pharmacy within that network. Here's why this is critical:

When using the Medicare.gov Plan Finder, you can also enter your preferred pharmacies to see how different plans interact with them, providing a more accurate cost comparison.

Understanding Deductibles and Cost-Sharing

Medicare Part D plans involve various forms of cost-sharing, and understanding these can significantly impact your out-of-pocket expenses. One of the most important components is the **deductible**. * **What is a Deductible?** A deductible is the amount you must pay for your prescriptions out of pocket before your Part D plan begins to pay its share. For 2024, the maximum Part D deductible is $545. However, many plans offer lower deductibles, and some even have a $0 deductible. * **How Deductibles Work:** If your plan has a deductible, you will pay 100% of the cost for your covered prescriptions until you meet that deductible amount. Once met, your plan will then start covering a portion of your drug costs, and you'll typically pay a copayment or coinsurance. * **Deductible Waivers:** It's important to note that many plans exempt certain tiers of drugs, often lower-cost generic medications, from the deductible. This means you might start