![[HERO] Medicare Advantage vs. Medicare Supplement: Which is Better for You?](https://cdn.marblism.com/DZf61VA7Jsd.webp)

If your mailbox looks like mine around enrollment season, you’re probably drowning in colorful flyers, "urgent" notices, and complicated charts. Everyone wants to tell you they have the "best" Medicare plan, but here’s the secret: there is no single best plan for everyone.

Choosing between Medicare Advantage (Part C) and a Medicare Supplement (Medigap) is easily the biggest decision you’ll make regarding your healthcare in retirement. It’s the fork in the road that determines how much you pay at the doctor, which specialists you can see, and whether you’ll need a separate plan for your teeth and eyes.

I’m Tim, and at VitalShield Insurance Services, we help folks navigate these waters every day. We’ve seen the good, the bad, and the "I wish I knew that before I signed up." Let’s break down the differences in plain English so you can decide which one actually fits your life.

What Exactly is Medicare Advantage (Part C)?

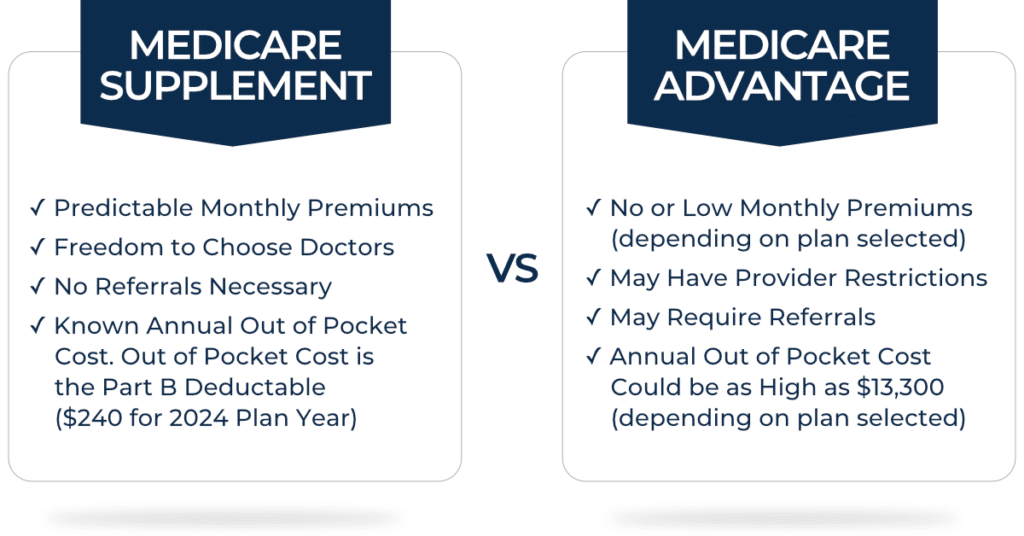

Think of Medicare Advantage as the "all-in-one" alternative. When you join a Medicare Advantage plan, you are still in the Medicare program, but you get your Part A (Hospital) and Part B (Medical) coverage from a private insurance company instead of the federal government.

These plans are structured a lot like the employer insurance you probably had during your working years. They usually include your prescription drug coverage (Part D) and often throw in "extra" perks like dental, vision, hearing, and even gym memberships.

The big draw? Most of these plans have very low: sometimes even $0: monthly premiums. But as the saying goes, there’s no such thing as a free lunch. You’ll pay copays or coinsurance as you go, and you usually have to stay within a specific network of doctors.

What Exactly is a Medicare Supplement (Medigap)?

Medicare Supplement insurance, often called Medigap, works differently. Instead of replacing Original Medicare, it sits on top of it. Think of Original Medicare as the foundation of a house and Medigap as the roof that keeps the rain (extra costs) out.

Original Medicare (Parts A and B) generally pays about 80% of your medical bills. You’re responsible for the other 20%, plus various deductibles. A Medigap plan "supplements" that coverage by paying some or all of those remaining costs.

With a Supplement, you keep your Original Medicare card, and the private insurance company just pays the "gaps." You have to pay a monthly premium for this coverage, but it provides incredible peace of mind because your out-of-pocket costs at the doctor are virtually zero.

The Great Debate: Pros and Cons

To really understand which one is better for you, we need to look at the trade-offs. It usually comes down to three things: Cost, Networks, and Perks.

Medicare Advantage: The "Pay-as-You-Go" Model

The Pros:

- Low Monthly Costs: Many plans have $0 premiums (though you must continue to pay your Part B premium to the government).

- Convenience: Your medical and drug coverage are bundled into one card.

- Extra Benefits: You get things Original Medicare doesn’t cover, like routine dental cleanings, eyeglasses, and fitness programs.

- Financial Safety Net: Every Advantage plan has a "Maximum Out-of-Pocket" limit. Once you spend a certain amount in a year, the plan pays 100% for the rest of the year.

The Cons:

- Network Restrictions: You usually have to use the plan’s network of doctors (HMO or PPO). If your favorite specialist isn't in-network, you might pay much more or not be covered at all.

- Prior Authorizations: You may need "permission" from the insurance company before getting certain procedures or seeing specialists.

- Variable Costs: If you have a year with a lot of health issues, those $20 and $50 copays can add up quickly until you hit that out-of-pocket maximum.

Medicare Supplement: The "Pre-Paid" Model

The Pros:

- Total Freedom: You can see any doctor, specialist, or hospital in the country that accepts Medicare. No networks. No referrals. No "permission" needed.

- Predictability: If you have a plan like Plan G, you know exactly what your medical bills will be. After you meet a small yearly deductible, you pay $0 for Medicare-covered services.

- Nationwide Coverage: This is huge for "snowbirds" who spend half the year in Minnesota and the other half in a warmer climate.

The Cons:

- Higher Premiums: You’ll pay a monthly bill for the Supplement plan, even if you never go to the doctor.

- No Extras: Medigap doesn't cover routine dental, vision, or hearing. You’ll likely need to look at standalone dental insurance for that.

- Separate Drug Plan: You’ll need to purchase a standalone Part D prescription drug plan.

Key Differences at a Glance

Which One is "Better"? (The Lifestyle Test)

Since "better" is subjective, let’s look at a few scenarios we see all the time at our offices in Blaine and throughout Minnesota.

Scenario A: The Budget-Conscious Senior

If you are on a fixed income and can't afford a $160–$400 monthly Supplement premium, Medicare Advantage is often the winner. You get dental and vision included, and as long as you stay healthy and stay in-network, your monthly costs stay low.

Scenario B: The Traveler or Snowbird

If you spend your winters in Florida or Arizona but your primary residence is in Minneapolis, Medicare Supplement is usually the way to go. You won't have to worry about whether a doctor in Scottsdale is "in-network" for your Minnesota-based plan. If they take Medicare, you’re covered.

Scenario C: The Person with Chronic Health Issues

If you know you’ll be at the specialist’s office three times a month or have a major surgery coming up, Medicare Supplement offers more predictability. You pay your premium, and the bills are taken care of. You won’t have to deal with the "sticker shock" of repeated copays.

Scenario D: The Person Who Values Convenience

If you hate carrying three different cards and paying three different premiums, Medicare Advantage bundles it all into one tidy package. It’s simple and straightforward.

Don't Forget the Enrollment Rules!

One of the biggest Medicare mistakes people make is thinking they can switch between these two options whenever they want.

In most states (including Minnesota), you have a "guaranteed issue" right to buy a Supplement plan when you first turn 65 or join Part B. After that window closes, if you want to switch from Advantage back to a Supplement later, the insurance company might put you through "medical underwriting." This means they can ask about your health history and potentially deny you coverage or charge you more if you have pre-existing conditions.

This makes the initial choice incredibly important. You aren't just choosing for this year; you might be choosing for the next twenty years.

Why Local Help Matters

You can call a 1-800 number and talk to someone in a call center halfway across the country, but they don’t know the doctor networks in the Twin Cities. They don't know which local hospital systems are feuding with which insurance carriers this week.

At VitalShield Insurance Services, we live and work right here. We understand the Medicare landscape in Minnesota because we help your neighbors every day. Our goal isn't to push you toward one plan or the other: it's to lay out the facts, look at your specific doctors and prescriptions, and help you find the fit that lets you sleep at night.

Ready to Find Your Perfect Fit?

The choice between Medicare Advantage and Medicare Supplement doesn't have to be a headache. Whether you're looking for health insurance options, curious about life insurance, or ready to dive deep into Medicare insurance, we’ve got your back.

Let’s chat! We can look at your current health needs, your travel plans, and your budget to see which side of the fence makes the most sense for you.

Click here to learn more about us or contact us today for a free, no-pressure consultation.

Medicare is a journey( don’t walk it alone!)